2024 Q1 Market Commentary…

The market finished off Quarter 4 of 2023 on a welcomed high note. Stocks and bonds got a significant lift from the talk of disinflation and potential interest rate cuts in 2024. The most overused term in finance – “soft landing” – is still the hope of investors going into the new year.

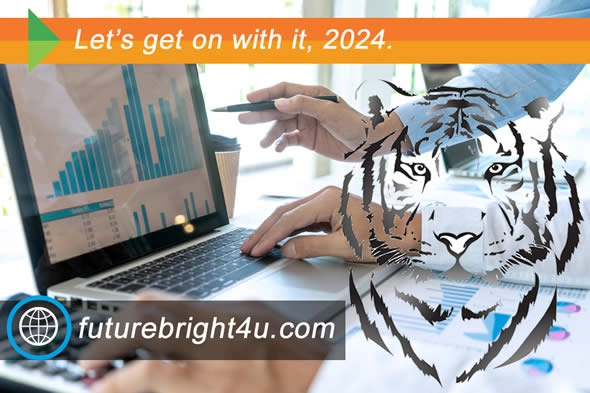

Speaking of the new year, I saw the perfect meme to describe, perhaps, the collective feeling of every American heading into 2024. It is a picture of a tiger laying in the grass enjoying a deep sleep until into the picture enters a man who sneaks up on the tiger ready to finger flick its tail. The caption reads, “Let’s get on with it, 2024.” Sometimes, a picture is worth a thousand words.

Managing assets through a macroeconomic lens should always garner the most attention, but there is a penchant from investors to try to predict market moves through the lens of politics in presidential election years. We hear the questions repeatedly on financial news networks day after day heading up to election day.

“How have markets performed historically in the final year of a president’s term?”

“How have markets performed when the incumbent party wins?”

“How have markets performed when the challenger party wins?”

“Will an unsettled geopolitical landscape present a “Black Swan Event” risk for markets?”

These are all valid questions, but they don’t really have substantive purpose because no predictable outcomes have been borne out of recent political victories or defeats. Therefore, without a consistent historical pattern to rely on, it’s just all conjecture. Conjecture is not a principle by which to create an investing thesis.

Even with uncertain and unpredictable outcomes, we do still need to adhere to an investment strategy for our clients. My wife has always been a believer in tackling big challenges by breaking them down into smaller chunks. She has mastered this approach, and I’ve learned from her over time. When applied to investing strategy, we can only work with what we do know to be true. We currently know the following:

• The bond yield curve is still inverted (US treasuries are paying you a higher rate for shorter term than longer term maturities).

• In December the S&P 500 Index regained its January 2022 high watermark line.

• Consumer spending rose 2.2% in 2023 but is trending lower for 2024.

• Inflation peaked at 7% in mid-2022 but is now back down to 3.1%.

• The Magnificent Seven stocks (AAPL, AMZN, GOOG, META, TSLA, NVDA, and MSFT) all returned much higher than long-term market average returns in 2023 but now carry historically high P/E (price over earnings) ratios.

Now, let’s break the data down into chunks and tackle each one…

Data: Treasury bond yield curve is still inverted.

Response: Own short-term treasuries, short maturity CDs and/or high yielding money market funds for fixed income allocations

Data: S&P 500 Index rebounded to January 2022 highs in late December.

Response: Maintain perspective that stocks are only back to where they started the year two years ago. Focus on future value, not just present value.

Data: Consumer spending rose in 2023 but is trending down in 2024.

Response: The consumer is responsible for 70% of U.S. economic growth. If asset values come down, consumers will tighten their belts in 2024. Under such conditions, we prefer holding companies with strong balance sheets, consistent earnings and revenue growth, and wide moats from nearest competitors. Thus, we favor large caps over mid and small caps.

Data: Inflation has decelerated significantly in the last year and a half.

Response: If consumers continue to reduce their spending, economic recession risk may become a reality. Historically, many market bull markets have started amidst recessionary conditions. Zoom out. Don’t jump ship when help is on the way.

Data: The Magnificent 7 stocks had outsized returns in 2023, so expectations are lower for 2024 returns.

Response: Understand that these seven companies garner a lot of attention and investment dollars for a reason. They are market leaders that continually reinvest profits into new, disruptive ideas and innovations. Current valuations can only account for what we see in front of us and represent only part of their future value. The work getting done in their research and development departments is what will drive future valuations. Unfortunately, we don’t always know what’s cooking behind closed doors. However, we have learned not to bet against companies with large pools of talent and rich balance sheets. That’s why we need to own them but also be on the lookout for those emerging companies that will one day join their ranks.

This is our playbook under current macroeconomic conditions. If you look at positions you own, your blend of asset ownership reflects our responses listed above. As is always the case, it is weighted commensurate to age and risk tolerance on a client-by-client basis.